How AWS and the collective knowledge of its immense partner network is driving innovation and sweeping changes in industrial technology

AWS re:Invent 2022 took place Nov 28 – Dec 2 in Las Vegas, Nevada. This was the 11th edition of the annual cloud conference which saw more than 50,000 AWS customers, partners, and employees participate, requiring six venues along the famed Las Vegas strip. Much of the content was also live-streamed online.

It was a massive conference with keynote speakers, product announcements, morning-to-night learning sessions, customer case study presentations, training and certification programs, a massive expo hall, hands-on technical labs, and walking, lots of walking.

By my count, 63 new AWS products and services were announced over the five-day event. Almost half of the solutions launched were in the Analytics (14) and Machine Learning (13) categories, but there were also announcements on Data Management Tools, Storage, Security, Compliance, Data Base, Networking & Content Delivery, Migration & Transfer Services, Developer Tools, Application Integration, Containers, Contact Center, Compute, and the big headline-grabber - AWS Supply Chain. With all that news, it would be easy to lose focus on the industrial solutions our LNS Research clients are interested in that align with our research coverage. Therefore, this article will primarily focus on AWS for Industrial and the smart manufacturing and supply chain topic areas.

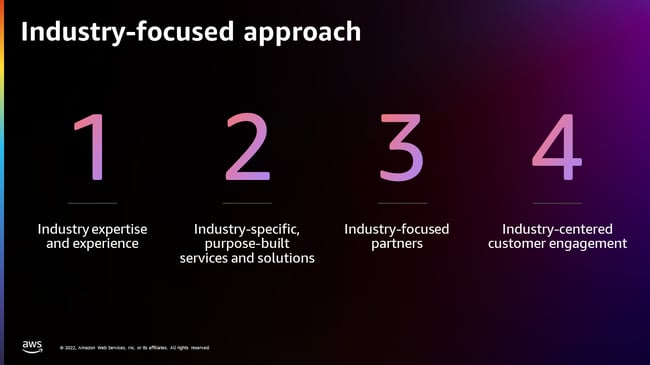

The industry-focused approach

With all the product and service announcements, partner and customer successes, cool demos, etc., it’s hard to name just one thing I learned at re:Invent that changed my perception of AWS, but for me, it was the intense focus on hiring industry experts with real-world experience. In fact, during the Analyst Summit at re:Invent in a session called AWS Vertical Industry Strategy, Josh Hofmann, Director of Business Development and Strategic Initiatives, presented the four pillars that defined the industry-focused approach. The predicate (Pillar 1) of the entire strategy has been to hire industry expertise and experience. Hofmann described the profiles as former executives, industry specialists, PhDs, and former factory leaders. “In every industry, we've hired these types of leaders, to help us deeply understand what our customers are trying to do and what use cases we can enable in each of the solution areas...These are people that come from industry. We choose industry first with the assumption that we can teach technology later, it's all about understanding the customer. They helped build and shape what we think the best solutions roadmap will be.”

Hofmann also noted that this strategy didn’t start in 2022, “I would point out that if you go around the company and you look at the leadership for our industries, our average tenure is around 7.7 years...this is something we've actually been doing for a long time. It's just now we're getting hyper-focused on how we expose all of this great work back to our customers, and particularly how we build our roadmaps.” This precept also mirrors LNS Research data on Industrial Transformation (IX) programs where “celebrity CDOs” struggled but successful programs are three times more likely to have program leaders with deep domain expertise. Fancy job titles don’t result in organizational adoption and program success.

Knowing there is this level of industrial experience, and it has been the baseline of the entire strategy is an important data point for both end users (buyers) out in the industry and for all the solution providers who have been cautious about how much of their limited resources they put into pursuing the AWS Partner Network. For example, the AWS Competency Program helps customers identify AWS Partners with deep industry experience and expertise, which is no small commitment. It is a rigorous validation process to establish a solution provider that has demonstrated relevant technical proficiency and has customer case studies with well-documented and verified return on investment (ROI) data.

These are the voyages of the Starship Amazon

These are the voyages of the Starship Amazon

In the immortal words of Captain James Tiberius Kirk, Why?

Why is AWS leaning so hard into this industry expertise and experience message? Some might say the obvious answer is to reinforce trust and credibility with customers and partners. Of course, but I think it's deeper than that. For years there has been an undercurrent of FUD (fear, uncertainty, and doubt) messaging aimed at the Hyperscalers, AWS in particular as the market leader, that these cloud infrastructure providers know their stuff when it comes to cloud computing, data storage, and now AI and machine learning, but they lack the industrial expertise and operations knowledge of how manufacturing, refining, power generation, Life Sciences, etc. “really work.” This means (the FUD continues) any project beyond their “core” cloud infrastructure scope will turn into a big science project requiring you to hire one of the big system integrator/consulting firms to come in and run the project, sending costs through the roof.

The FUD industry lives in the shadows of the technology world much like its evil twin in politics, using operatives (who call themselves industry consultants), the internet, and “publications” to drip narratives into the marketplace. Thus, it made total sense to me when I heard Josh Hofmann say, “It's just now we're getting hyper-focused on how we expose all of this great work back to our customers, and particularly how we build our roadmaps.” Hofmann and the leadership at AWS may not focus on or care too much about the FUD operations out there, but this presentation at re:Invent was a brilliant refutation.

Build and Partner

With the industry expertise and experience established with Pillar 1 of the AWS strategy, Pillar 2 “Industry-specific, purpose-built, services and solutions” delivers detailed industry-specific roadmaps that directly address customers' needs, down to their specific use cases. A clear and natural outcome leveraging all the expertise they have assembled and reflected in solutions like AWS IoT TwinMaker (for Digital Twins), Amazon Lookout for Vision (for Quality), and Amazon Monitron (for machine condition monitoring and predictive maintenance). Pillar 3 “Industry-focused partners” is all about the ever-expanding 100,000+ AWS Partner Network. In 2022 we saw a significant increase in engagement with AWS from LNS Research solution provider clients and those that regularly brief us including Seeq, Element, Tulip, and MachineMetrics, to name a few.

-

-

-

Seeq just achieved AWS Life Sciences Competency status after previously earning AWS Industrial Software Competency in 2019 and AWS Energy Competency in 2021.

-

Tulip announced the launch of Computer Vision for Quality Insights, powered by AWS, a new solution that allows manufacturers to integrate machine learning-powered defect detection.

These are examples where LNS Research has a line of sight into what is required and how to navigate the AWS Partner Network, including how to take advantage of the resources AWS has made available for partner enablement. This is not unique to AWS obviously. Both Microsoft Azure and Google Cloud have partner programs and most technology suppliers are not exclusive, taking an agnostic approach with the Hyperscalers. However, after reviewing the details and speaking with many solution providers at re:Invent, it is clear that AWS has significantly increased its investment in growing and supporting its partner program - leading with free online training content to educate and equip partners for success. AWS has tracked over 13 million people accessing these online course modules with a goal to train 29 million for free by the end of 2025.

Co-innovation

The final Pillar in the AWS strategy is Industry-centered customer engagement. Both Josh Hofmann and Grant Bodley, General Manager of Industrials & Manufacturing, discussed the guiding principle of offering manufacturing customers “step-change improvements rather than incremental ones” and that sometimes requires co-innovation with industrial customers directly. One example presented at re:Invent was Carrier, the world's largest producer of cold chain equipment. AWS worked with Carrier to look across the entire cold chain value chain, which includes grocery delivery, pharmaceutical delivery, and use cases to protect against spoilage and waste. The result was Lynx, a connected cold chain digital logistics solution that delivers real-time visibility and insights about the journey of temperature-sensitive cargo.

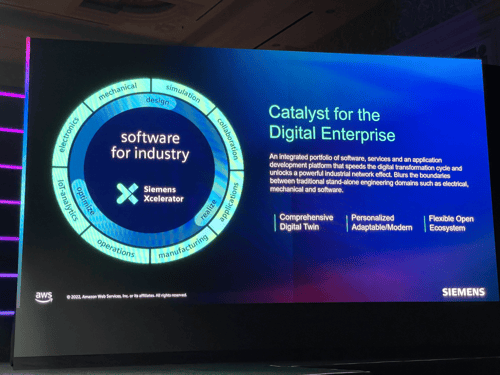

The eight-year collaboration with Siemens was also a reoccurring theme in the industry content at re:Invent. Tony Hemmelgarn, CEO of Siemens Digital Industries Software presented on Siemens Xcelerator software for industry and working together with AWS on application development tailored to the cloud. This includes microservices, everything from IoT to IT-OT convergence to a next-generation MES, and how Siemens leverages AWS IoT TwinMaker to assure a comprehensive Digital Twin. Hemmelgarn concluded his remarks by emphasizing that “most of our applications now are available on the AWS Marketplace for our customers to be able to purchase easily.”

Siemens Xcelerator - Software for the Industry

Siemens Xcelerator - Software for the Industry

Tony Hemmelgarn, CEO of Siemens Digital Industry Software

Tony Hemmelgarn, CEO of Siemens Digital Industry Software

Siemens rightly listened to their customers who wanted the simplicity of AWS Marketplace, which, along with Microsoft’s Azure Marketplace, are the only ecosystems that have achieved critical mass and captured mind share with CIOs. Where ERP vendors held favor over the past decade, now industrial software vendors are leveraging the Hyperscaler online marketplaces in a win-win-win. The transaction happens on the AWS or Azure marketplaces, the end users like the simplicity enabled to purchase and deploy, and for software vendors, it upends the old paradigm of long sales cycles associated with enterprise deals.

AWS Supply Chain: Leveraging what Amazon has learned since its founding in 1994

The preview of the new AWS Supply Chain solution at re: Invent brought the history of Amazon and Amazon Web Services full circle. From July 1994, roughly 28 years ago, when Jeff Bezos started amazon.com in his garage as an online marketplace for books, data and the tools to learn from that data started to grow. Today AWS customers can leverage all that learning by deploying AWS Supply Chain and its machine learning models, pre-trained with all the years of supply chain management and optimization experience that helped amazon.com grow into the $500B business it is today.

We saw a preview of some of these supply chain capabilities at the Amazon re:Mars conference a few months prior when PepsiCo and AWS partner Provectus presented a detailed case study that included e-commerce demand planning as part of an initiative on transformation through data and machine learning. The ability to generate more accurate demand forecasts is directly connected to meeting customer promises and core functionality in AWS Supply Chain.

Adam Selipsky, CEO of AWS, identified that from a customer engagement standpoint “big horizontal use cases” like with AWS Supply Chain, will produce higher-level conversations and relationships. Supply chain disruption is a global issue, a “CEO-level agenda item” Selipsky said. “I think that to a large extent, we've just moved so much further up the layers of our customer organizations over the past few years, just because of how fundamentally important AWS has become to them.”

Does adding the “horizontal” product strategy to the 4 pillars of the vertical industry strategy elevate deal discussions from the functional and operational leadership up to the C-suite? We’ll see. It’s a sound and logical strategy with some proof points, but AWS Supply Chain is a new product, so I’ll be looking forward to the data on how many customers buy and implement it in 2023 and 2024, and the benefits they document.

Challenges ahead

With the economy in, or at least on the verge of, recession as we enter 2023, the year may be a bit more challenging than Adam Selipsky forecasts. When asked about the possibility of an economic slowdown impacting AWS growth during the Q&A with the analysts at re:Invent, Selipsky answered that the business “will continue to, I think, accelerate...”

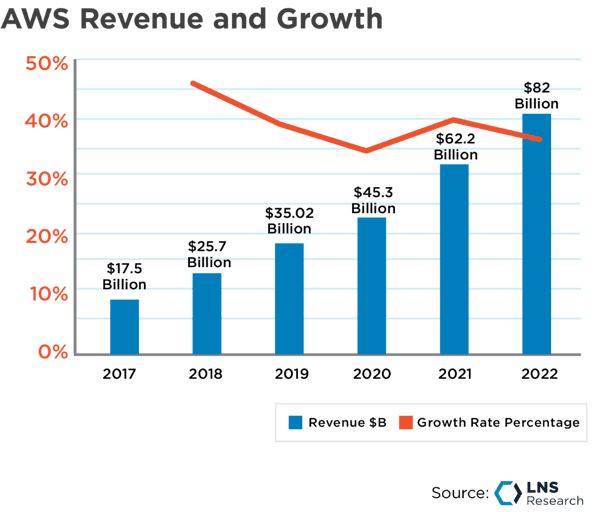

Was that answer confidence or rosy optimism? Every time the naysayers and skeptics predict doom, AWS puts another year of 30%+ growth in the books. AWS has achieved a 36.5% average annual growth rate over the past 5 years.

Parent company Amazon, however, is responding to the economic conditions. What was reported in November to be a reduction in headcount of 10,000 has grown to a total of 18,000 workers in January. While there is no reported direct impact or layoffs announced for the AWS business, the cuts at Amazon will be used by AWS competitors to try and create uncertainty.

Conclusions

“AWS is becoming a cloud operating system,” said the text message from my LNS Research colleague Niels Andersen, one of the many watching the re:Invent sessions online. That text message took me back to 2007 when Steve Jobs introduced the iPhone and completely altered the future of personal computing and communications. There are many parallels from that era in tech history and how AWS and the collective knowledge of its immense partner network are driving innovation and sweeping changes in industrial technology today.

This concept of a cloud operating system would be a path to true interoperability across applications, would drive the Industrial Data Hub, and bring together third-party infrastructure players to enable a “system of systems" where an operating system (OS) is system software that manages computer hardware, software resources, and provides standard services for computer programs. We are seeing the emergence of Cloud Operating Systems (COS) that manages the same types of resources across a cloud infrastructure. Such interoperability is the vision end users have expressed through organizations like OPAS, NAMUR, and CESMII.

If there is an economic slowdown, the diversity across the 15 AWS industry segments will help lessen the impact if a recession causes retraction in the manufacturing and industrial segments LNS Research focuses on. AWS' business in Financial Services, Telecommunications, the Public Sector, Media & Entertainment, and Healthcare would likely see a secondary impact, if any at all, allowing them to retain their position as the leading provider of cloud services.

According to Synergy Research Group, AWS is the cloud services market leader with a 34% global share, followed by Microsoft Azure at 21%, and Google Cloud at 11%. The latest LNS Research data from our State of IX Tech survey (to be released in Q1 2023) has a narrower scope representing our industrial/manufacturing research universe. Our data indicates a more even ranking amongst the Hyperscalers with AWS still the market leader by over 8%, but with Microsoft Azure and Google Cloud virtually tied.

The competitive landscape will continue to be intense and end users will benefit from that healthy competition. As Josh Hofmann said, “it's all about understanding the customer.”

All entries in this Industrial Transformation blog represent the opinions of the authors based on their industry experience and their view of the information collected using the methods described in our Research Integrity. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with or endorsement by them.